Why Trading an Unwanted Gift Card Beats Selling It for Cash

Why Trading an Unwanted Gift Card Beats Selling It for Cash

We've all been there. Someone gifts you a card to a store you never shop at, you've got a leftover balance after a return, or some promo code lands in your inbox for a brand you don't care about. First instinct? Sell the card and get cash. Makes sense on paper — money is money, and you can spend it however you want.

But once you actually run the numbers, the picture shifts. In most cases, trading the card for a gift card to a store you actually use is the better move than selling it for cash. Here's the breakdown.

1. The resale space is loaded with scams

Reselling gift cards is one of the sketchiest corners of e-commerce. A few of the classic plays you'll run into as a seller:

- Chargeback after delivery. Buyer pays, gets your code, drains the balance, and a few days later disputes the charge with their bank. Money goes back to them — your card is empty.

- The "let me verify the balance" switch. Buyer asks you to send the code "just to check it," redeems it on their own account, and tells you the card was dead on arrival.

- Fake middleman sites. Cloned versions of well-known platforms pop up, you drop your card into "escrow," and the site disappears overnight.

- Disputes on legit marketplaces. Even on real platforms, it's nearly impossible to prove a digital code was working when you sent it. Digital goods basically can't be "returned" in any meaningful way.

Even when you use a big-name resale platform with seller protection, the risk of having your payout frozen or held during a dispute is always higher than a direct card-for-card swap.

2. Platform fees: 5–10% off the top

Any site that helps you sell a card takes a cut for listing it and handling the transaction. Rough market averages:

| Service type | Typical fee |

|---|---|

| Dedicated resale platforms | 5–10% |

| General marketplaces | 7–15% |

| Direct buyback from a service | 15–30% (off face value) |

So on a $100 card, you're already down $5–$10 just for the privilege of using the platform.

3. Payment processing: another ~4%

When your buyer pays with a credit card or through a payment service, the processor takes their cut too — usually 3–4%. That fee almost always falls on the seller (the platform pulls it out of your payout) or gets baked into a steeper discount on the listing price.

Add in cashout fees to move the money to your bank account (another 1–3% depending on the method), and the total drag on a single transaction easily hits 10–15% of face value.

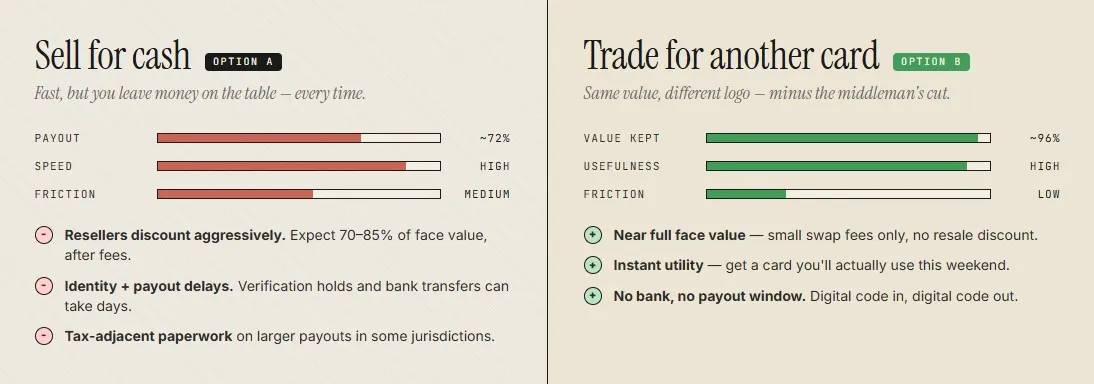

4. The actual math: here's what you lose

Let's run a real example. Say you've got a $100 gift card to a popular store. Selling it looks like this:

| Step | Amount |

|---|---|

| Face value | $100.00 |

| Market discount (−10%) | listed at $90.00 |

| Platform fee (−7%) | −$6.30 |

| Payment processing (−4%) | −$3.60 |

| Cashout fee (−1%) | −$0.80 |

| What you actually get | ≈ $79.30 |

| Total loss vs face value | ≈ 21% |

So even on a liquid card to a major retailer, you're walking away with around 20% less than the card is worth. And that's the best-case scenario — no scams, no disputes, no frozen funds.

5. Why trading cuts through most of this

When you swap one card directly for another:

- No payment processing. No money is moving between cards or bank accounts — only digital balances are being shuffled around.

- No cashout fees. You don't need to pull anything out to a bank. You get a usable asset on the spot.

- No commission skimmed from your balance. This is where a free platform changes the math entirely. On FlipGift there are no fees, no commissions, and no premium tiers taking a cut — the full value of your card stays with you. (Here's exactly how a swap works.)

- Way lower scam risk. Trades happen instantly and automatically through the matching engine — you're not negotiating codes with a stranger on the internet.

Even when the exchange rate isn't 1:1 (say one store's card trades for another at 0.9), you're still walking away with a balance you can actually spend — not a chunk of cash that's already been gutted by fees and still needs to be spent somewhere.

6. When selling actually does make sense

To be fair, trading isn't always the right call. Selling for cash makes sense when:

- you've got a niche card to some small store and nobody's offering a trade for it;

- you specifically need the cash, not a store credit (like, you need to cover a bill);

- the balance is tiny — a few percent in fees on a $15 card just doesn't matter;

- you've got a trusted offline buyer (a friend, a coworker) and no middleman is involved.

Outside of those cases, treat trading as your default option.

Bottom line

Selling a gift card looks like the most direct way to turn something unwanted into money, but in practice it's the path with the biggest leaks: market discount + platform fee + processing + scam risk. Stack those up and you're easily looking at a 15–25% hit on the face value.

Trading for a card you'll actually use strips out almost all of those costs and leaves you with real spending power that's close to what the card is actually worth. Before you list a card for sale, take a look at the live pool and see if you can just trade it for something you were planning to buy anyway. Nine times out of ten, you'll come out ahead.